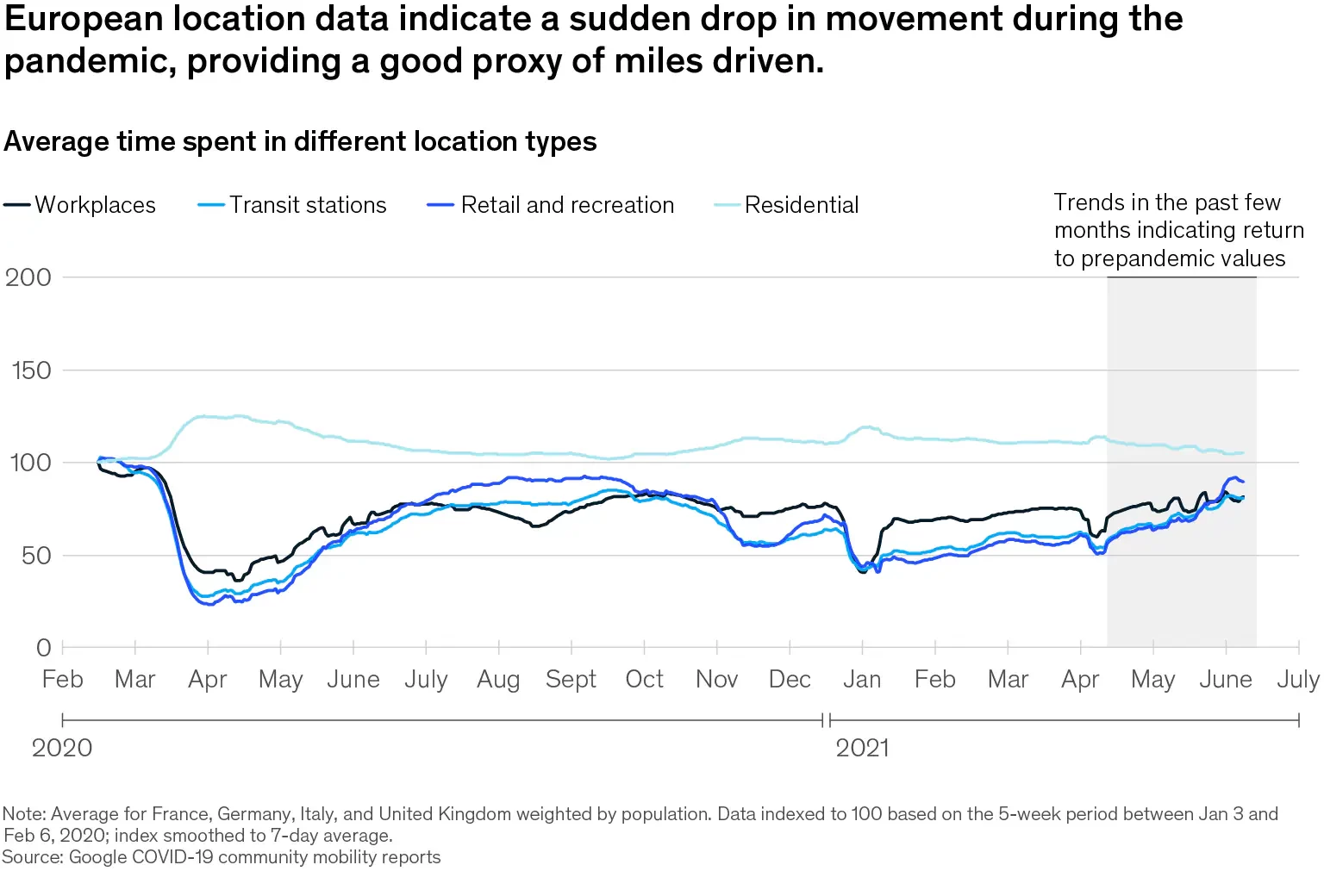

The epidemic has caused extraordinary disruption to the insurance industry as a whole, drastically reducing company activity and upsetting employees’ and customers’ daily lives, among other things. Companies that draw a significant percentage of their revenue from car insurance, on the other hand, have had stronger bottom-line results during the pandemic than in prior years. Because claims dropped by 60 to 80 percent virtually immediately when abrupt lockdowns kept drivers at home and off the road (see exhibit). Once limits were eased, claim volumes increased, though they are still 20 to 30 percent lower than before the pandemic. The associated decline in claim payouts was only partially compensated by premium refunds offered to consumers to compensate them for flying less miles.

Motor claims volume stays suppressed as of mid-2021—at least for the time being. This provides an opportunity for insurers to undertake or accelerate strategic initiatives aimed at developing claims excellence, a fundamental driver of profitability. Among these initiatives include the transformation of claims processes to improve customer experience, the development of digital capabilities, the use of sophisticated analytics to better decision-making, and the reduction of long-standing sources of leakage. Acting now will help insurers be ready when vaccination rates accelerate across Europe, economies reopen, and both mobility and motor claims recover.

Changes in the claims environment

Even when the pandemic has passed and business resumes, insurers will face three chronic difficulties that can be addressed—at least in part—by modernising claims administration to boost profitability.

The pressure on the top line will remain. Top-line pressure from the pandemic is anticipated to persist for the foreseeable future. If history is any guide, commercial lines that were temporarily halted in the tourist, aviation, entertainment, and local business sectors may be difficult to recover. After the 2008 financial crisis, for example, business lines recovered much more slowly than personal lines. In terms of personal lines, decreased commuting has changed customers’ perceptions of the value of insurance: if they drive less, they anticipate to pay less. As previously stated, several insurers have proactively provided their customers premium paybacks for reduced car usage—a trend that may continue.

Digital technology is here to stay. People switched numerous daily operations to distant channels and adopted new digital tools as a result of the pandemic. For example, in Europe, 60 to 70 percent of consumers switched some of their shopping online, and the majority want to keep the new habit when the pandemic is over. This shift in customer behaviour included interactions with insurance. During the pandemic, digital claims notifications more than doubled in the United Kingdom, and insurers got 30% more digital enquiries than in the prior. Customers’ increased expectations for an end-to-end digital experience—with 24/7 assistance, rapid feedback, and a user-friendly interface—remains a challenge for most insurers. The vast majority of clients still prefer to call rather than use digital self-service; in Europe, for example, more than half of all claims are launched by contacting an agent. This choice may imply that insurers have failed to fully digitise the claims process.

Inflation will have an impact on claim expenses. Insurers expect growing pressure on claims expenses from a variety of sources. First, auto repair shops have suffered as a result of the COVID-19-induced decline in claim volume. Many received government assistance, but they also increased labour rates and profit margins on spare components. The claims inflation rate is currently between 4 and 5%. Due to ongoing cost pressures, repair shops are unlikely to revert to pre-COVID-19 pricing levels without substantial industry reform. In one possibility, insurers could take on the role of ecosystem orchestrators, dramatically aggregating repair volumes and providing strong incentives to repair shops to participate, such as extending insurance benefits to encompass maintenance and offering negotiated prices for components and labour. Likewise, insurers can utilise larger volumes of claims data to continuously monitor repair shop performance and then use those insights to lead clients to the best bargains.

The future plan for claims

Even before the epidemic, insurers had made significant advances towards improving their bottom lines by enhancing productivity and optimising technical quality, particularly through pricing. It is now time to deal with allegations. Claims firms can take advantage of the lower claims volume to plan strategic investments in advanced analytics transformation, develop new digital talent initiatives, and better understand customer wants and expectations.

The new claims and customer experience model is built on a comprehensive suite of analytics and updated process automation, both of which are required for precise, end-to-end automation. The tools are improving, enabling automated decision-making throughout the claims processing process, including routing, triaging, responsibility negotiation, cost estimation, determining whether to repair or write off damaged vehicles, cash payouts, and fraud detection. All of these areas will increasingly rely on digital and analytics rather than manual labour, transforming the entire claims operating paradigm.

A primary focus is to respond to client needs for a flawless claims process. Customers are hungry for and accepting of new digital experiences, as seen by the epidemic. They expect complete transparency throughout the claims journey; minimal effort on their part (for example, very little back and forth with the agent to resolve the claim and receive payment); faster claim resolution, possibly including automated payments; and the ability to move seamlessly between the digital and physical worlds.

Insurers can also try to limit leakage and boost their bottom line. Leakage can take many forms, such as replacing a vehicle rather than repairing it, providing a luxury replacement vehicle rather than a car that matches the customer’s vehicle class, and expending money for in-person loss assessments even in clear circumstances where images would suffice. To combat leaks, enable fast detection of anomalies, select claims for comprehensive investigation, and empower claims organisations to close claims that cast no doubt.

To achieve these key goals, a move from a fragmented and frequently segmented approach based on unintegrated digital and analytics technologies to end-to-end digital and analytics-enabled claims processes will be required. On the front end, insurers will need to provide tools that are comparable to the top digital services that their clients use every day (for example, ride-hailing apps, social media, and digital banks).

To save costs, claims organisations will need to invest in a portfolio of analytics engines to assist automated decision-making. The opportunity begins with claims prevention—using telematics and the Internet of Things to issue safety warnings and damage prevention tips—and extends throughout the claims processing journey, from providing customers with a simple digital first notice of loss interface and improving claims cost accuracy, to digital repair shop selection and automated payment processing and invoice checks. This relative lull in activity also provides insurers with an excellent opportunity to equip claim teams with the training they require to master new processes and operate new digital technologies.

Claims are already on the rise, so insurers’ time is running out. Developing end-to-end digital and analytics solutions will demand significant investment and time. It is vital for claims organisations to act quickly or risk losing the potential to emerge from the epidemic stronger than competitors.